Starting with the A´s...

Get ready for the first trip to the german small cap jungle. Stock Safari in the german SDAX - Part 1

If you want to discover interesting ideas in investing that are not popular yet, there is no alternative but starting with the A´s, as Warren Buffet once pointed out. My plan is, to screen the german small cap sector and write a short paragraph about every company. If I think a company fits my investment scheme, it will be put on the watch list.

1&1 Drillisch (2,2 bil € Mcap)

1&1 is a german provider for telecommunication services and broadband. It is a special company, because 78% of the shares are owned by United Internet AG. This is actually a nice success story, the founder Ralph Dommermuth is is a self-made german entrepreneur. They decided in 2019 to bid for the 4th german 5G license and are currently building their own 5G network in germany, which requires a lot of capital-investment. It is a stable business but competition is fierce and their revenue is growing more or less with inflation. This is a red ocean strategy and the stock price reflects just that. Maybe things will change with the 5G network, but this is beyond my circle of competence.

Valuation is cheap, P/E TTM is 6,4, but I will pass.

About You (828 mil € Mcap)

This is an interesting one! Former german E-Commerce poster child, unicorn with a celebrity founder (Tarek Müller). Checked all the boxes of the 2021 market and went public for 23 € a share. All investors that sold directly made a small buck, but those that went in for the long run suffered so far.

They have a lot of cash and are still in “unprofitable growth” mode with negative earnings / free cash flow. Guidance is 10%-20% YoY revenue growth for FY23. Their main business is online retail which is a tough market with strong competitors (Zalando, Asos, brands like adidas and Nike switching to DTC). Inventory is piling up (more than doubled YoY) - that´s usually bad for a fashion company.

They have a SAAS business with the SCAYLE platform that is rapidly growing (66% revenue growth. Not sure if this will be their future.

The shareholder structure is also a problem. 63,5% of the shares outstanding are owned by OTTO, a german retail powerhouse. There is only 21,2% free float. Maybe at some point, the main shareholder will take advantage of the depressed stock price and take the company private again?

All in all not my cup of tea, I will pass.

Adesso AG (659 mil € Mcap)

This company flew under my radar for the last 10 years. Bad for me. They are an IT service provider with 800mm revenue in 2022. They focus on Germany but have subsidiaries in many other european countries. No hype stock but a consistent creator of shareholder value:

If you bought them ten years ago and sold during the covid peak, you would have made 30x your money, excluding dividends. Valuation seems reasonable, although not cheap at 23 TTM P/E. I need to dig deeper to understand their secret sauce and future growth perspectives.

This is a watch.

Amadeus FiRe (528 mil € Mcap)

This is a personnel service provider with a funny name. There is a lot to like here. They grew revenue quite consistently over the last years from 137mm in 2012 to 372mm in 2021. Operating margins were stable at around 16%, only covid was a problem but they recovered quickly. The balance sheet and RoA suffered in 2019 when they bought ComCave GmbH, a specialist for adult education. I have to do more analysis here. Although the company seems solid, it´s not super attractive and outside my area of competence.

I will pass.

Atoss Software (935 mil € Mcap)

A software developer and consulting company for workforce management, time logging, employee integration etc. Strong double digit growth over many years, but current P/E of 48 is very high compared to 2018 when it was valued at a P/E-Range between 15-18. I might be wrong, but this company seems fairly valued at best in my opinion. Therefore I pass.

Auto1 Group (1,4 bil Mcap)

A loss-making german “tech startup” that buys and sells used cars and went public at the peak of the stock-mania in 2021 at an incredible valuation of 7.9 billion €! Since then, the stock went downhill and I cannot see that the business model will ever work out. Fantastic IPO timing, though! I will pass.

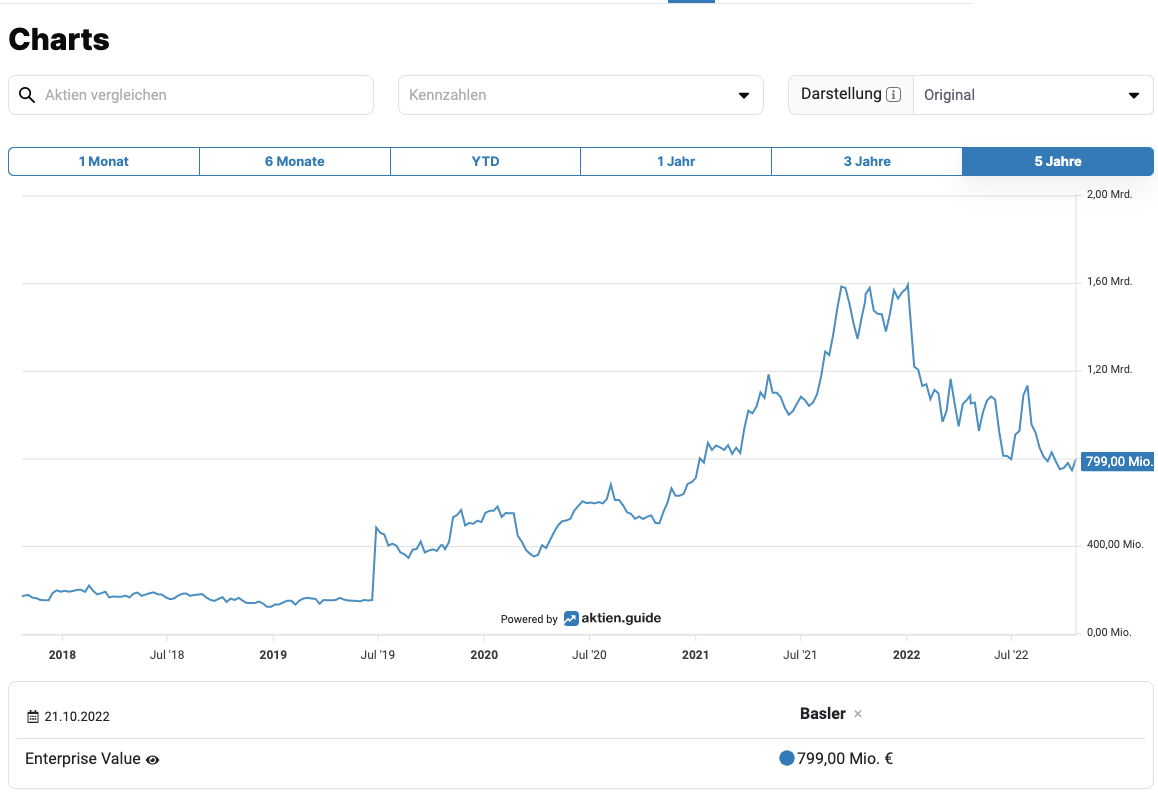

Basler AG (736 mil Mcap)

A german hidden champion that develops camera software and technology. They call it “computer vision” and this was quite a success story if you look at the 10 year stock chart:

Although the stock price collapsed from it´s covid high of around 160, substantial value was created for long-term shareholders. The stock chart is misleading, because they did a capital increase from company funds in July 2022, increasing the stock outstanding 3-fold but that did not dilute shareholders. So it might be better to look at the chart of the enterprise value:

Revenues were constantly increasing over the last years, although not very smoothly. There seems to be a cyclical element to the business. I personally think that demand for “computer vision” should increase in the future and will analyse the company in more depth. The insider ownership is really high, north of 50%! Valuation is still not cheap at a P/E of around 30.

I will watch this one.

Baywa (1,5 bil Mcap)

Baywa is a well diversified company that is active in three main areas. Their energy business is segmented into “Energy” which is the legacy business that sells oil & co. and “renewable energies” where they sell components and do projects in PV and wind farms. Revenue growth in H1 was 66% and EBIT is up more than 100% due to the current energy crisis in germany. Their agricultural business unit sells fertilizers, seeds and equipment and is also doing really good at the moment. Then, there is building materials, where they also had a nice growth of 17% in revenues and 30% in EBIT.

Due to their business model they have very thin operating margins with a lot of cyclicality, but they managed to be profitable in the last 10 years. Management seems to be doing a good job, but I personally think that the upside is limited at the current valuation. Looks a a cyclical business near its peak. I will pass.

Bilfinger SE (1,1 bil Mcap)

Bilfinger is a multinational service provider in the construction industry. They changed their business model in the recent years, more service, less construction activity. The share price is down 60% from 10 years ago, they seem to struggle and at a current P/E of this company looks 9 fairly valued. I have no edge here and will pass.

Cancom (930 mil Mcap)

Cancom is an IT service provider and offers IT products and services in Germany and internationally. Revenues were growing nicely but have been hit hard in 2020 and have since not recovered fully. There is significant goodwill and intangibles on the balance sheet and return on capital is quite low (7%) in recent years. I will pass.

That was it for now. The next 10 stocks will follow soon.