German SDAX shares part 2

German SDAX shares part 2

here we go from Ceconomy to Eckert Ziegler

Ceconomy (Mcap 704,54 Mio. EUR)

Ceconomy operates retail stores and ecommerce stores for consumer electronics in europe under the brand Media Markt, Saturn, iBood and Juke. They are struggling for obvious reasons. As a (mainly) brick and mortar retailer, they are under constant attack by “your margin is my opportunity” Jeff Amazon. The stock price is near all time lows, their margins are deteriorating further. One could bet on a recovery, but their structural problems are here to stay. Also very heavy debt, this is a dangerous situation for the company.

There are some positives though, online sales are now 25% of total sales and revenue is rising, although only 3,6% in the last trading update.

I have no edge here and think there are better turnaround situations in the market right now. I will pass.

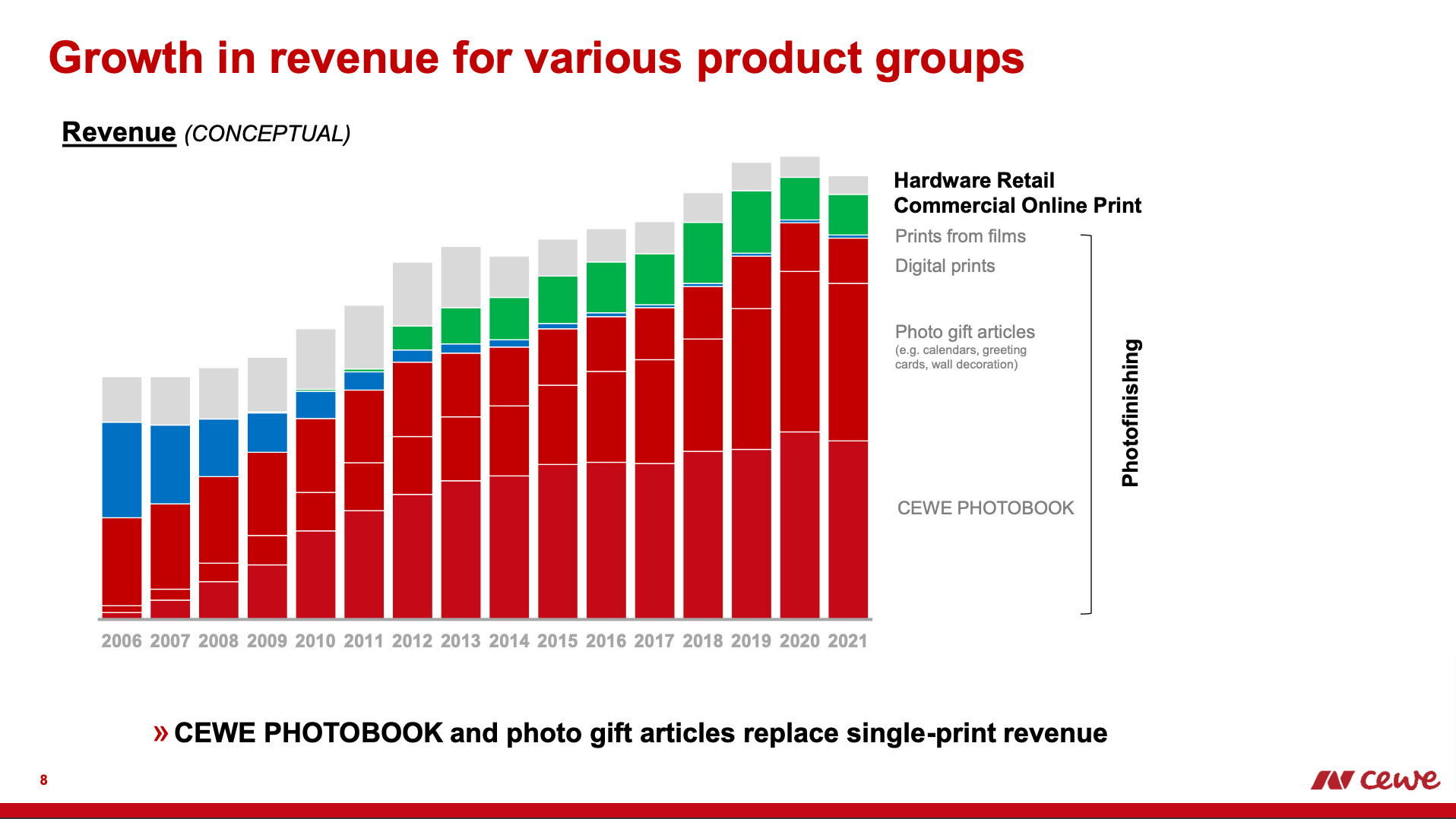

CEWE Stiftung (Mcap 574,28 Mio. EUR)

CEWE is an interesting company, a real survivor! They once were Germanys biggest “prints from film” company, a classic photo shop with many outlets all over the country. They nearly got killed due to the shift to digital cameras in the 2000s. Due to good management, they survived the transition, reinvented themselves and are now in a good position. The main product is their photo book that you can order online. Basically a printed book with photos from your last holiday, your children, etc. I am a customer myself and like the product. They also sell photo gifts and have a growing “commercial online print” division where they bought Saxoprint, a big online printshop a few years ago. Commercial online print is a tough market with fierce competition (zero moat) that is not growing, I doubt that this will be their future.

I think they are underestimated and have a moat around their photo book and photo-printing franchise. There are switching costs for the consumer if he orders his photobook somewhere else (different software, lost uploads to the CEWE platform) and their photo-terminals are everywhere in supermarkets and drugstores in Germany.

The ownership structure is interesting, 28% of shares outstanding are owned by insiders and the founder family. They think long term, which I like. They have little debt and margins are increasing. They are a very consistent dividend payer, current yield is around 3%. Covid reopenings/more travel and the fact that more photos than ever are taken via smartphones should be a long term tailwind.

My only concern is that growth is absent at the moment. They need to find ways to increase revenue. If they don´t, the current P/E ratio of 12 is fair and not cheap. But I am optimistic, they had revenue declines in the past, e.g. 2013-2014 and were able to get on track again.

I will watch and investigate.

CompuGroup Medical (Mcap 1,94 Mrd. EUR)

Compugroup is a dominant player in the healthcare software area. They develop software for medical practices, pharmacies, laboratories and hospitals. The founder Frank Gotthardt stepped down as CEO in 2020, so the new guy Dirk Wössner has to prove himself. They are a growth story and acquisitions have played an important part in their growth. They have a lot of long term debt, 800 Mio. The equity ratio is still OK at 32,93 %, but one has to keep in mind that 2/3 of the balance sheet are intangibles and goodwill.

They are not loved by their customers. I know doctors that complain about their software, I have no idea whether the problem is behind or in front of the screen.

This one goes into the too hard pile, I will pass.

CropEnergies (Mcap 1,33 Mrd. EUR)

CropEnergies is one of the few stocks that are up in the current environment. They produce alternative fuels (bio ethanol) that is in high demand. In the end, this is a commodity business that is highly influenced by political decisions (e.g. how much bio ethanol will be added to the fuel at the gas stations). I have zero edge in this market.

Therefore I will pass.

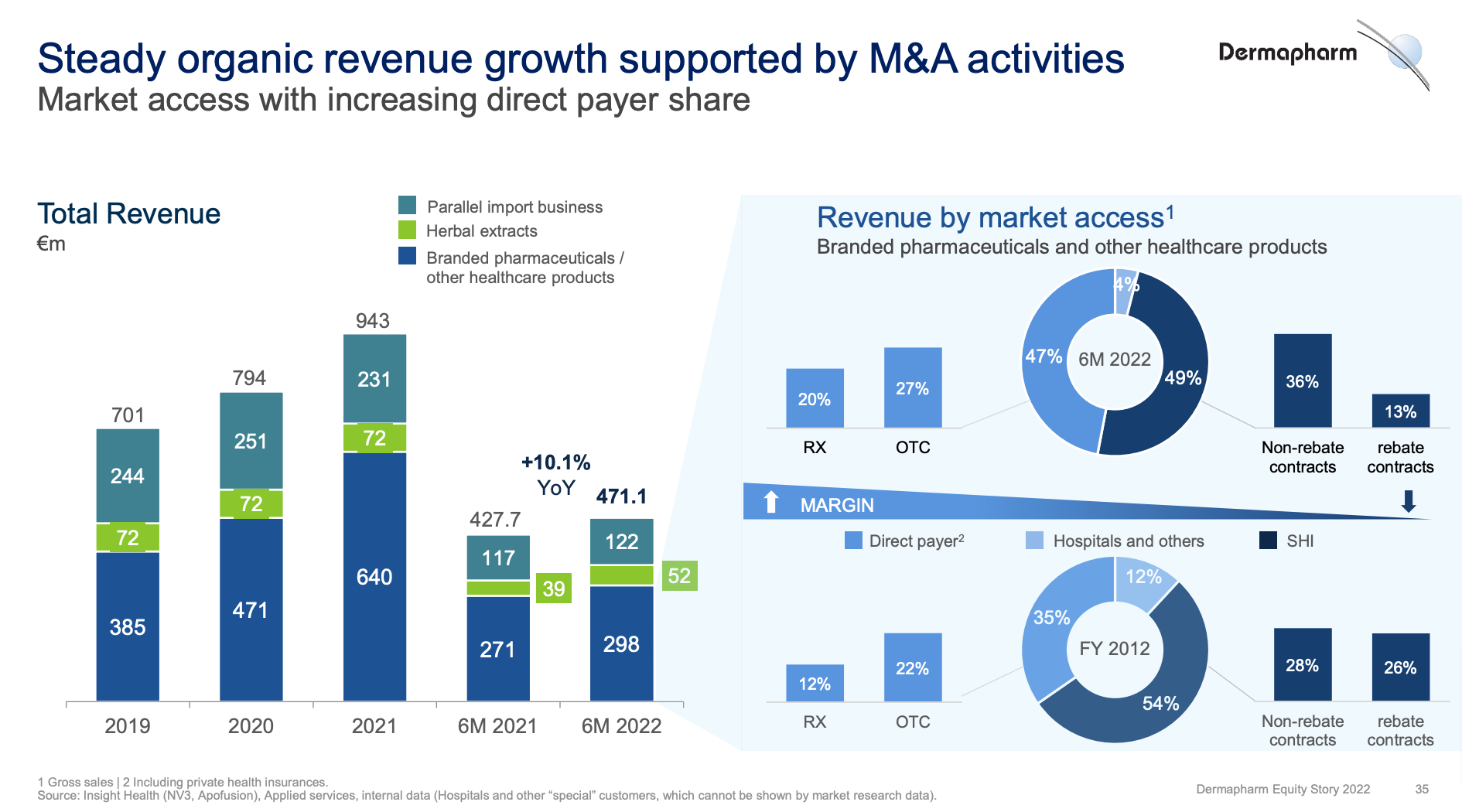

Dermapharm (Mcap 2,14 Mrd. EUR)

Dermapharm is a double digit growing manufacturer of branded pharmaceuticals in Germany, with a huge variety of brands and products. Some of their products are household names, like Dekristol or Vita Aktiv B12. The product range and pipeline looks interesting. Gross margins and operating margins are improving, the LTM operating margin is at 30%. The stock price shot up during covid because they are a licensed producer of the Pfizer/Biontech vaccine. Vaccine production stands for approx 20% of the current revenue. Since the peak the stock more than halved and looks really interesting at a P/E TTM of 11. Dividend is at 5%!

Even if they are/were overearning due to the vaccine production - they look very attractive. Am I missing something? A quick scuttlebut check of the bulletin boards brought up some concern because the CFO left suddenly in September. A new CFO will start in November. On the other side, there are insider buys from the CEO.

For me, this is a clear watch candidate. This could be a “Davis Double”, a growth stock that is currently priced like a non growing dividend stock. So in the best case, you get EPS-growth + multiple expansion.

DEUTZ AG (Mcap 453,96 Mio. EUR)

This is a classic german engine building company. They manufacture Diesel engines, Gas engines etc. Free Cashflow is low compared to earnings, I think this is your typical capital intensive business with limited growth prospects and continuous reinvestments of earnings to stay in business. The stock chart reflects that:

I will pass.

DIC Asset AG (Mcap 612,00 Mio. EUR)

DIC Asset AG is one of Germany's many listed real estate companies, and specializes in commercial real estate. They crashed with their peers recently and are now at 2015 price levels:

The CEO is Sonja Wärntges, and it´s sad that a female CEO is still something remarkable in the current german business-sphere. For me this is a positive, since there are studies that show superior leadership and investment behavior of the female gender.

The company trades at half book value, quite cheap at first glance. The dividend yield is north of 10%. However, the looming interest increases are troubling. They have to refinance debt all the time.

They have a diversified portfolio of office-, logistics- and retail-buildings. They took over their competitor VIB Vermögen AG, a specialist in the logistics space in 2022. It is hard for me to value these kinds of companies because their balance sheets are really “flexible”. One example: A quick check reveals, that their takeover target (VIB Vermögen AG) adjusted their portfolio value literally weeks after the acquisition from 1.5 billion (31.12.2021) to 2.3 billion (1.4.2022). That seems strange and subjective at best. A devils advocate might think they needed more “substance” in the balance sheet to get better financing terms?!

I think they are cheap but I would need to dedicate a lot of work to understand the balance sheet, the financing terms etc. Additionally, I am pessimistic for office space due to the “work from home” trend. I see no real tailwind here. Too hard pile for now, I will pass.

Drägerwerk AG (Mcap 776,66 Mio. EUR)

Drägerwerk AG is a manufacturer of equipment for hospitals, industry and fire brigades. They are the leading producer of ventilators and this was the reason the stock spiked during covid. However, the longterm performance of the stock is not good. No real value for the shareholder was created in the last 10 years:

I am not an expert in this field and will pass.

DWS Group (Mcap 5,38 Mrd. EUR)

The DWS Group is an asset manager and is more or less a subsidiary of Deutsche Bank, the biggest german bank owns 80% of the shares. They are in “value territory” now. P/E TTM stands at 7, the dividend yield is 7.5%. Revenues from fees are up approx. 30% since the IPO in 2018 and margins are increasing. However, the stock price is down.

The current bear market will have a negative effect on their fees, OK, I can see that. But markets will rebound, as they always did and people in Germany are well aware that they need to invest for retirement, so I think they will continue to see inflows from existing and new clients. The Q3-22 report was OK, assets were stable compared to last year (despite stock market declines) but costs were up a little. They should control costs better, but I think they know that already.

The current trend in investing is passive index funds and DWS has those too, but the active funds play a much bigger role for them. The fear is, that Blackrock and Vanguard are coming for them. I see that problem, but I think it´s overstated and well priced in. They have some kind of moat because the salespeople in the banks are still incentivized to sell DWS funds. I read many times, that funds are very sticky once invested in a vehicle. So I really think they are currently mis-priced and will watch them because I see some revenue growth and a potential multiple expansion.

Eckert Ziegler AG (Mcap 849,22 Mio. EUR)

Eckert Ziegler is a manufacturer of very special medical equipment in nuclear medicine and radiation therapy. I knew that nuclear medicine is helpful in treating thyroid cancer, but Eckert and Ziegler seems to be a specialist in eye cancer and prostate cancer. The company has an interesting history, the founders were east german scientists who became entrepreneurs in 1992 and have grown the company organically.

The stock is really volatile, more than a 20-bagger in 10 years and then a 70% decline in the last 12 months. I really wonder why they went up this much, because revenues and EPS merely trippled during the last 10 years. Anyway, the stock is not cheap at P/E TTM 30 and although they seem to be a good company I doubt they will be a good investment at that price. I will pass.

That´s it for now. To be continued…