El.EN - stock analysis (ELN)

El.EN - stock analysis (ELN)

An Italian company with growth at a reasonable price in laser technology

Hello dear reader,

I plan to share more of my stock analysis on this substack in the future, so here we go with a quick analysis of El.EN, a stock that I like and recently bought for my portfolio.

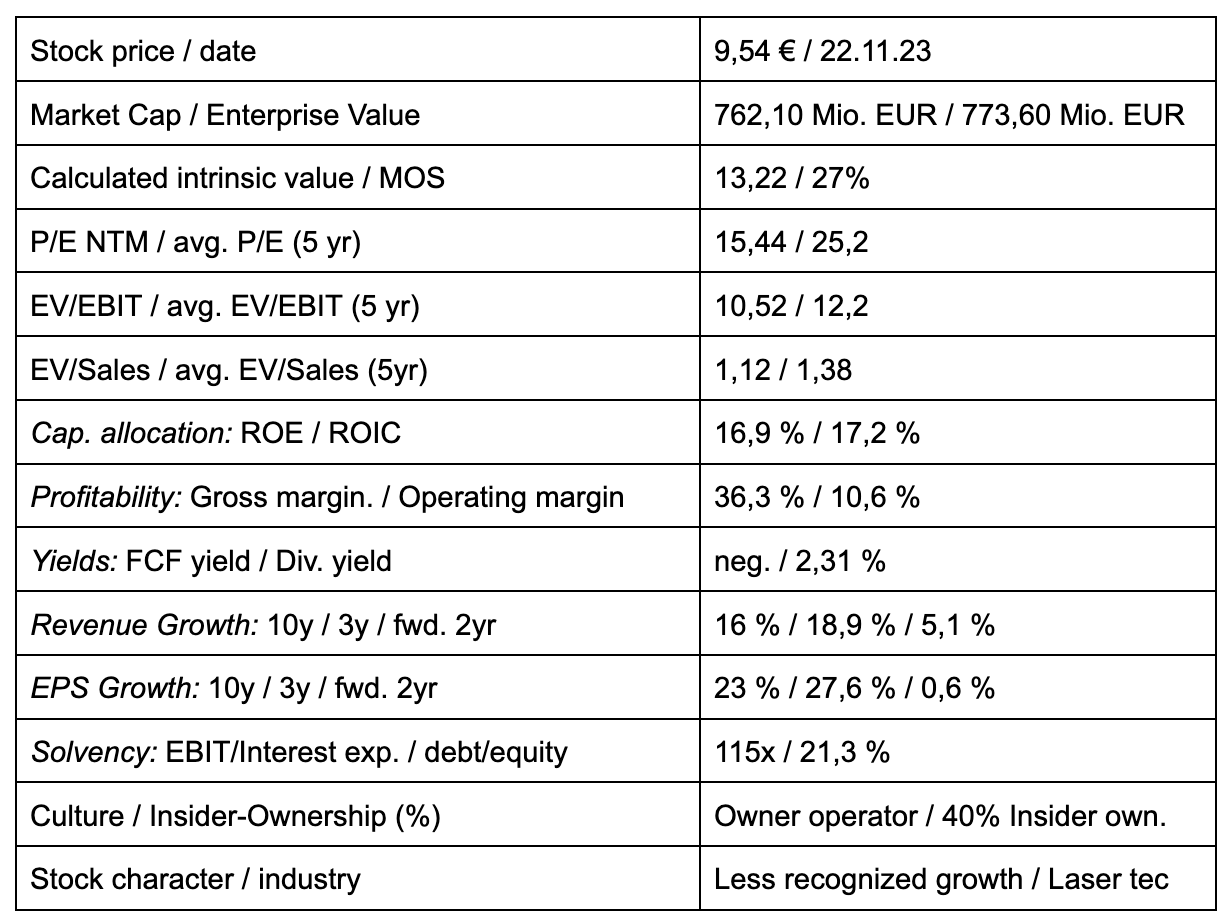

I will start my analysis with some key statistics:

This is what the stock did in the last 10 years, not too bad:

My investment thesis

ELEN is an Italian quality company with a good market position in a growing industry. The stock price suffered from multiple contraction recently, due to declining growth estimates and (I hope) temporary problems in their Chinese division.

Nevertheless, this is an industry leading owner-operator company in an industry with secular growth that can be bought for a modest P/E of 13. The management is product-driven and long term oriented.

Time should be our friend here.

The company

El.En is an Italian company that is a manufacturer and distributor in laser systems for medical and industrial use and in conservation/restoration laser solutions.

The company name stands for “Electronic Engineering” and was founded in 1981 out of university by the engineer and professor Leonardo Masotti and his best student Gabriele Clementi, who is the current CEO. As you would expect from two engineers, the company is product- and research driven and has built up a reputation for good products and solutions.

El.EN has a global presence and manufacturing facilities in Italy, Germany and China.

They have a multi-brand strategy and sell their products under various labels: Asclepion, DEKA, Quanta Systems, Renaissance, Penta Chutian, Cutlite, etc.

They have a wide product offering with very different use cases. From industrial precision laser cutting to tattoo removal to restoring vaginal health. There are so many use cases.

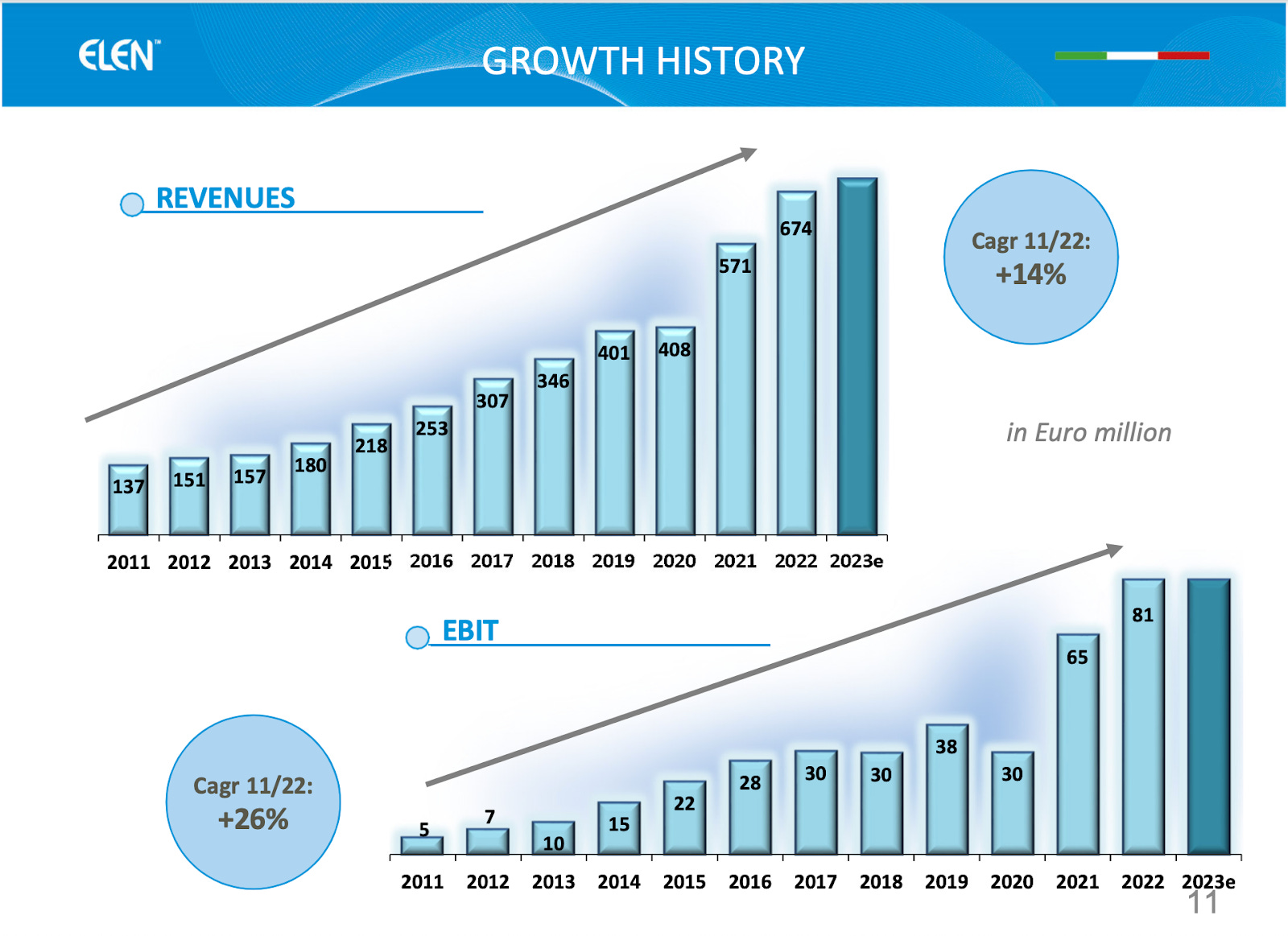

They are in constant growth mode, revenue and EBIT rose with double digit CAGRs in the last 12 years:

I personally think that we can expect the company to grow further in the coming years, as their medical (growth estimate 13-15%) and cosmetic (growth estimate 15-19%) laser end markets are estimated to grow at double digit CAGRs to 2030. For the industrial laser market, growth of around 9% is estimated to 2030. The company grows organically but is also an active consolidator and grows by acquisitions. The acquisition targets usually are treated as separate entities and their brands and structures remain.

Business model and Moat

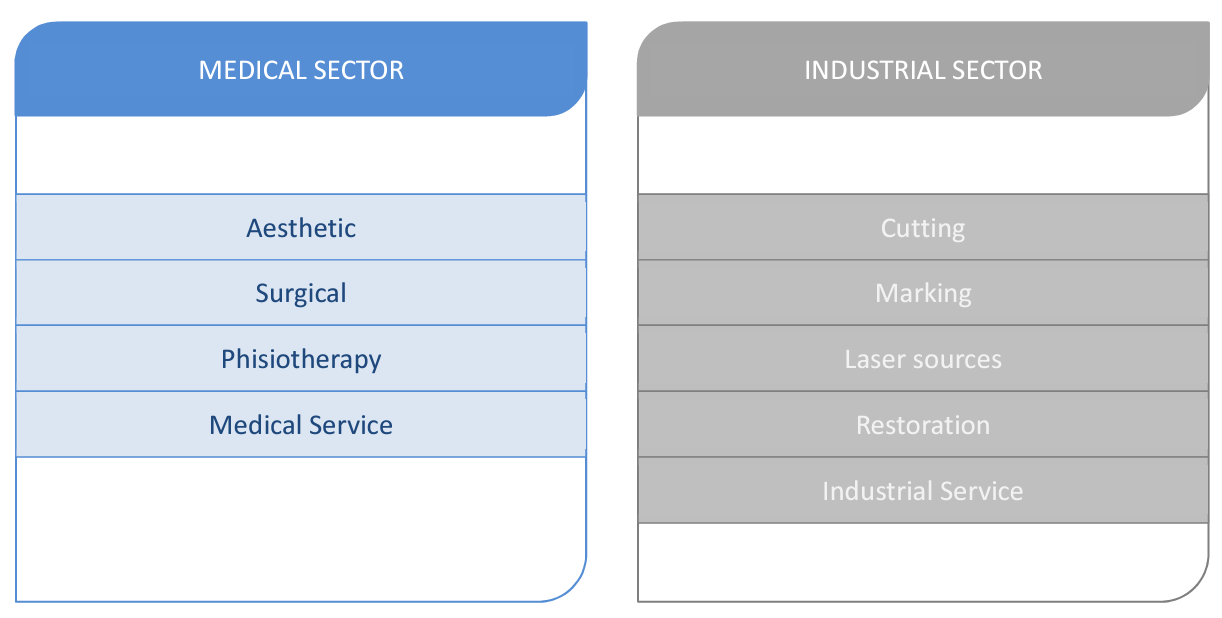

The company produces lasers primarily for medical and industrial applications:

The company employs 180 research engineers and spent €20 million (around 8% of gross profit) on R&D last year. I like that and I think this is necessary to keep innovating and coming up with new products and solutions.

A cyclical element is there, because the revenue on product sales of the new devices can be impacted by a recession or product cycles, but the company also generates a regular stream of income through spare parts sales, service and maintenance, but this revenue only represents 13 % of total revenue.

The company is divided into many small divisions, some of which were acquired and each specialize in serving a sub-segment of the market. This is a deliberate strategy, as the CEO claims, that they can make more customer focused decisions this way and stay entrepreneurial.

The rather low gross margin of 36% suggests that a significant proportion of components are purchased and not manufactured in-house.

I think the moat comes primarily from three sources and I see a bigger moat in the medical and cosmetic field:

technical know-how/advantage through the extensive R&D activities and patents

branding-power and customer retention - a customer who is used to their products will probably remain a loyal customer

regulative barriers to entry, we are talking about medical products in their medical branch

But this business is not a blue ocean, there are several competitors in medical lasers, like Candela Corp, Cutera or InMode and also in industrial lasers like IPG Photonics, Trumpf, Raycus or Lumibird.

Management, incentives, ownership

This is where the company can shine, the original co-founder Gabriele Clementi is still on board as CEO, over 40% of the shares are in the hands of the owners. As shareholders, we are fully aligned.

In the annual report, the remuneration of the entire Board of Directors is stated as €1 million annually, which is absolutely within limits.

This company is not an enrichment scheme for managers, but a life's work of two engineers that are passionate about technology and their lasers. In their conference calls, they talk about the numbers in a professional manner, but when they get a chance to speak about new products, the tone sounds really enthusiastic:

Growth from new products is the best way to grow, and that's exactly what they are doing.

Key numbers from QuickFS

The business is slightly cyclical, not recession immune (see 2009-2011), but clearly growing nicely

ROIC and ROE are OK and improving

margins are improving

What is particularly outstanding is the sales growth and the strong balance sheet

Valuation

My conservative estimate of intrinsic value is significantly below the current price, the MOS is 27% in my opinion. We have the opportunity to invest in this company at an entry multiple of around 10x EV/EBIT. Future growth is an important part of the investment thesis, but the company has proven that it can grow by achieving a 14% CAGR of revenue and a EBIT CAGR of 26% since 2011.

Risks

In the last big recession after the GFC, the company was hit hard and it took them 3 years to recover. That shows that they are not recession immune (cosmetic spending is discretionary, industrial spending depends on business conditions), but with no debt and good management, the patient investor can sit things out.

They currently have problems in the Chinese market that declined in 2023. They are open about it and want to fix that, but China is currently a minefield for many companies. In the last conference call, they are talking about fierce price competition. Industrial lasers are growing less than the rest and currently stand for 40% of revenue, but this is still a serious threat.

Net working capital ballooned in 2023, the explanation is that in 2022, they were struggling to source materials (remember COVID?), so they ramped up inventory AND reduced payment terms for creditors. I think this is understandable and was a reasonable business decision at the time, that will reverse in the next quarters. This already reversed a bit in the last quarter, but I should watch it.

Regulatory risk: When you look at the chart, you will notice a massive drop in 2018 which was caused by a dispute between the FDA and the company about marketing material for their mona lisa touch vaginal rejuvenation product. These regulatory issues can come out of the blue and we as investors will have no control about it.

They are dependent on continuous innovation and new product creation. The company culture and the management seem to be product driven and passionate about engineering. But this should be constantly watched.

Conclusion

I want to simplify things and the companies that I want to own long term should pass my simple checklist:

Is it a good company? Yes, I think so, because the company has good returns on capital, an innovative company culture and an owner/operator as CEO. The company has a reasonable moat, but needs to defend that moat continuously.

Is the company financially healthy? Yes, they have no debt and are profitable.

Can I buy it at a good price? Yes, the current multiple is below historic averages and a P/E of 13 and an EV/EBIT of 10 are absolutely reasonable

Is there a potential for growth? Yes, their end markets will grow double digits in the next couple of years and the company has demonstrated good growth in the past

Can the stock deliver a 10-12% annual return in the next 5 years? Yes, I think it is very likely that the stock can deliver that return because I get a high shareholder yield and double digit growth on top with more likelihood of multiple expansion than multiple contraction.

In summary, El.EN is an interesting company that can currently be bought well below historical average valuation multiples and has a long runway for growth. It is not perfect (no Coca-Cola type business), because the moat depends on continuous innovation and successful product development, but risk/reward seems good in my opinion.

This is a stock for an investor with a long time horizon, the return will mainly come from long term revenue and earnings increases and only partly (if any) from multiple expansion. The stock needs attention and if there are signs that the company loses it´s engineering mojo, the thesis is broken.

Therefore, the stock is a buy for me and I allocated 3% of the portfolio to El.EN.

Sources:

https://www.valueinvestorsclub.com/idea/El.En._SpA/9837645495

https://elengroup.com/uploads/relazioni_e_bilanci/Half_yearly_Financial_Report_2023.pdf

TIKR

Disclaimer

I do hold an investment in the issuer's securities.

Nothing on this substack is investment advice.

The information in this article is for information and discussion purposes only. It does not constitute a recommendation to purchase or sell any financial instruments or other products. Investment decisions should not be made with this article.

The information contained in this article is based on generally-available information and its accuracy and completeness cannot be assured.

Investments in financial instruments or other products carry significant risk, including the possible total loss of the principal amount invested.

What do you think about the loss in competitive edge within sheet metal cutting in China (industrial division)?